A Conceptual Model for Personalizing an Automated Teller Machine

This article introduces a new conceptual model for automated teller machines called the personal bank teller. The disadvantage of the conceptual model users have of current automated teller machines is of an inflexible mechanical replacement for a bank teller. The personal bank teller aims to personalize automated teller machines by controlling the options that are offered and the order in which they are displayed, and by insulating the user from the differences between domestic and international automated teller machines. Design considerations for an implementation of personal bank tellers are discussed.

1. Introduction

This article introduces a new conceptual model for automated teller machines (ATMs) called the personal bank teller. The personal bank teller personalizes ATMs to individual users by controlling the options that are offered and the order in which they are displayed, and by insulating the user from differences between domestic and international ATMs.

Section 2 describes the disadvantages of the conceptual model of current ATMs. Section 3 presents the new conceptual model, and section 4 discusses hardware, software, and storage considerations for an implementation of personal bank tellers.

2. The Current Conceptual Model

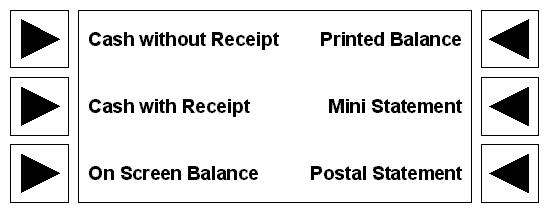

The user interface of a typical ATM contains a list of around six to eight options. Each option is presented on the screen next to the button that invokes the option. The following diagram shows the layout of an ATM with six common options. The interaction with the user interface of an ATM involves inserting the ATM card, selecting options from an on-screen menu by pressing the (hardware) buttons next to the options, typing PIN numbers and cash amounts on the keypad, taking cash and receipts, and receiving the card.

The conceptual model that users have of current ATMs is of a mechanical replacement for a bank teller that provides a limited and generic set of bank services. Users interact with impersonal and inflexible cold, hard technology that affects the interaction in many ways. For example, users are regularly reminded of this inflexibility because the ATM card must be inserted in one (arbitrary) orientation of eight possible orientations.

The main disadvantage of current ATMs is that they cannot be personalized to individual users. Users have no control over which services are offered. Each time the customer uses an ATM, the services that are never used are still listed on the screen and the frequently used services are still relegated to a secondary screen of options. ATMs never learn which options the customer needs and which ones they do not.

The next section describes a replacement for the inflexible technology conceptual model with a flexible personal assistant that learns about the needs of the user.

3. A New Conceptual Model

Many bank customers regularly visit their local branch. Customers build up a relationship with the bank tellers; they may even have a favorite teller. The tellers get to know the customer; they get to know which accounts a customer holds, the details of their mortgage or personal loan, and what kind of transactions the customer is likely to perform.

The new conceptual model is a personal bank teller (PBT) that travels with the user on the ATM card. The PBT personalizes an ATM to the needs of the customer. Customers will no longer be using a machine; they will be interacting with their PBT. Each customer’s PBT is unique to that customer. Over a series of interactions with an ATM, a customer’s PBT builds up a model of the services that are regularly chosen and the information that is regularly requested.

The PBT is based on the concept of an interface agent (Crowston and Malone 1988). Laurel (1991) defines interface agents as “computational characters that assist and interact with people.” Interface agents can perform mundane scheduling tasks, customized information searches, and can provide companionship, help, and advice. The tasks performed by the PBT interface agent are those of presenting relevant information to the user in an order that enables the user to use that information more effectively. The PBT also takes care of tasks that would be undertaken by a real personal assistant, such as providing translators from the local language to the customers language, and insulating them from the problems encountered in different domestic and foreign environments.

One characteristic of an interface agent is that it is “capable of taking actions on behalf of users” (Laurel 1990). The PBT interface agent is more suited to a support role that enhances the options available to the customer when they use an ATM. The PBT does not take any action on behalf of the customer for two reasons. First, it requires a level of trust that customers may not be willing to give. Second, ATM transactions need to be performed by the customer because they need to read balances and take cash from the machine. An interface agent that acts on behalf of the customer would be more suited to a desktop banking application for ordering bank statements and cheque books, for example.

Some interfaces use anthropomorphism to present their conceptual model to the user. The Guides system, for example, is a multimedia database of American history from 1800 to 1850 (Oren et al. 1990). The guides, an Indian chief, a settler woman, and a frontiersman, each have a life story that enables them to relate the history of the period from their point of view. Each guide is represented by a picture of a person dressed in a typical outfit of the time. Anthropomorphic characters such as an Indian chief can help to explain the conceptual model of the system. Laurel’s (1990) explanation of why we personify interfaces is that “computers behave. Computational tools and applications can be said to have predispositions to behave in certain ways on both functional and stylistic levels. Interfaces are designed to communicate those predispositions to users, thereby enabling them to understand, predict the results of, and successfully deploy the associated behaviors.” The interface of a PBT could use anthropomorphism by presenting a picture of a bank teller on the screen. The choice of whether the bank teller is male or female can be made by the user. The user might also be able to choose a specific bank teller from a virtual staff of tellers. User selection reinforces personalization.

The PBT uses a model of the customer to personalize ATMs by controlling which options are offered and the order in which they are displayed, and by insulating the user from differences between domestic and international ATMs by roaming.

3.1 Controlling Content

The PBT is able to tailor the content of an ATM to each customer so he or she is not restricted to a generic set of services. For example, if the customer regularly withdraws cash, most of the options on the initial menu screen will correspond to cash. Other services would be grouped together and accessed via a secondary screen of options. Similarly, if a customer regularly requires other services, for example viewing their balance or ordering a statement most of the initial menu options would relate to these services with the cash withdrawal options relegated to a secondary screen.

Because the bank knows about the customer’s accounts, mortgages, loans, etc. the PBT is able to offer current information about these products. If a customer has a mortgage or a personal loan, the PBT would provide further options relating to these services. If the interest rate on a mortgage has changed, for example, the user would be given the option to view the interest rate or request other literature to be sent to their home. Customers without a mortgage or loan would not be given these options.

3.2 Ordering Options

One of the ways a PBT can personalize the user interface of an ATM is to control the order of the menu options that it has decided to present. For example, if the most frequently withdrawn amount is £15, this would be the first option listed, followed by the less frequently chosen amounts. Similarly, if balances were requested more frequently than statements, the balance option would be displayed first. Placing the most frequently used options near the top of the menu will reduce search times and make option selection less error prone. Optimizing the order of the options should reduce the time taken for a transaction because the customer is able to access the most frequently used services more quickly. In an evaluation of a telephone directory menu system, Greenberg and Witten (1985) found that users liked its adaptive menus that placed the most frequently used telephone numbers first.

Greenberg and Witten did not consider whether such changes would disorient users and make the interface harder to learn. In a study of a pull-down menu of food items, in which frequently selected items migrate to the top, Mitchell and Shneiderman (1989) found that users were unsettled by the changes and performed better with static menus. ATM menus, however, are much shorter than the menus in computer applications, and the amount of time that passes between using an ATM is long enough to enable the position of the options to change without causing confusion.

To be sure there will be no confusion, when the customer begins to use his or her PBT, a number of transactions with an ATM need to be recorded to build up a pattern of regular use. Until there is a clear pattern to influence the order of the options, the standard ATM order should be used. This will ensure that the layout of the ATM screen will not vary noticeably from transaction to transaction.

3.3 Domestic and International Roaming

The PBT travels on the ATM card wherever the customer goes. The information displayed by an ATM is dependent on the customer’s PBT, not the ATM. The PBT insulates the customer from the differences between different ATMs at home and abroad. Any anxiety about using an ATM in a foreign country should be reduced.

Whichever ATM the customer uses in whichever country he or she visits, the PBT ensures that the ATM displays the options in the customer’s language. A German tourist visiting the UK would operate an ATM in German whereas a Japanese businessman visiting France would operate an ATM in Japanese. The cultural difference of writing from top to bottom in columns would be handled by the PBT: a Japanese PBT knows how to display Japanese.

As far as possible, the options presented by the PBT in different countries will be the same as on ATMs at home. The currencies would differ, but the PBT would be able to convert the amounts usually requested by the customer into the local currency.

4. Design Considerations for an Implementation

This section discusses design considerations for three aspects of an implementation of PBTs: the hardware, the software, and the storage of the information required by a PBT.

4.1 Hardware

No changes to the hardware of ATMs should be necessary to implement PBTs. The PBT conceptual model does not change the basic interaction with an ATM that involves selecting options from an on-screen menu and typing PIN numbers and cash amounts on the keypad.

Although the languages and character sets might differ between countries, the ATMs in current use around the world use very similar hardware with bit-mapped monochrome or colour displays that are able to display diverse character sets such as Latin (English) and its variants (French, German, etc.), Cyrillic (Russian), and Kanji (Japanese).

4.2 Software

Major changes to the software would be required to implement PBTs. Each bank would need to implement a software architecture for PBTs. Agreements between domestic and international banks would also be required to implement the domestic and international roaming features of a PBT. Agreements such as Cirrus already exist that provide limited co-operation between banks worldwide for withdrawing cash.

4.3 PBT Storage

The amount of information stored by a PBT would depend on its complexity. For example, a simple preference of cash over other services would require just a single bit. More preferences would require more storage.

The magnetic strip on an ATM card does not have the capacity to store the information required by a PBT. However, it is becoming more common that ATM cards are smart cards that have the capacity to store application data. Smart cards remove the need for the bank’s database to store the information for a PBT. ATM preferences are specific to each user and are only used when interacting with an ATM so it makes sense to store this information on the card.

References

- Crowston K. and T. W. Malone, “Intelligent Software Agents”, Byte 13(13), 1988: 267-274.

- Greenberg, S. and I. H. Witten, “Adaptive personalized interfaces: A question of viability”, Behaviour and Information Technology 4(1), 31-45: 1985.

- Laurel B., “Interface Agents: Metaphors with Character,” in The Art of Human Computer Interface Design, Brenda Laurel (ed.), Addison Wesley, 1990.

- Laurel B. Computers as Theatre, Addison Wesley, 1991.

- Mitchell J. and B. Shneiderman, “Dynamic versus static menus: An experimental comparison”, ACM SIGCHI Bulletin 20(4), 33-36: 1989.

- Oren T., G. Salomon, K. Kreitman and A. Don, “Guides: Characterising the Interface,” in The Art of Human Computer Interface Design, B. Laurel (ed.), Addison Wesley, 1990.